Smart home products and systems are increasingly influential in attracting buyers across different price points.

>34% of likely buyers would pay a few thousand dollars extra for a smart home compared to a non-smart home.

~85% of buyers consider smart home features important, with ~40% expecting to pay no additional cost.

Homeowners who are looking for ways to access cash in their home without having to refinance to a higher rate than what they currently have can explore their home equity options. These include home equity loans, which come with lower interest rates than other credit types and a tax deduction on the interest paid, and HELOCs, which have variable interest rates and allow borrowers to deduct up to 80% of their home equity.

Everyone is talking about home prices and the affordable housing crisis. A lot of people are wondering, or even think home prices are going to crash, mostly thanks to reporting from the media. But where are home prices headed for the end of 2023 and beyond? First, let’s look at where home prices are at the moment and how we got here.

The rate of increase in home values has been massive during the last two years. While this has resulted in enormous equity gains for homeowners, it has also led some home buyers to fear that home prices may decline. It’s critical to understand that the housing market isn’t a bubble ready to burst, and that home price increase is being sustained by solid market fundamentals.

Check out our video about home price forecasts from now till 2027:

To understand why price decreases are unlikely, it’s necessary to investigate what caused recent price increases and where analysts believe home prices are headed. Here’s what you should know.

Home Prices Rose Significantly in Recent Years

Mostly thanks to the pandemic prices rose dramatically. Money was cheap, as in you could borrow money at very low rates, at 3% or lower. People suddenly had to switch from working at an office to working at home and these homeowners discovered they needed a home office. Some people either realized or couldn’t deal with the lack of space with the entire family being at home and needed more room just to have some breathing room or private time. As a result, people were buying houses left and right, bidding wars ensued and prices went through the roof. That puts us at where we are today with high home prices but with much higher mortgage rates.

So What’s This Mean If You’re Considering Buying A Home?

If you’re thinking about purchasing a house, you’re probably paying attention to everything you hear about the housing market. You get your information from a variety of sources, including the news, social media, your real estate agent, talks with friends and family, overhearing someone talking at the grocery store, and so on. Most likely, home prices and mortgage rates will rise significantly.

Let’s take a look at the statistics to help you cut through the noise and get the information you need. As you make your selection, here are the top two questions you should ask yourself about home pricing and mortgage rates:

Where Do I Think Home Prices Will Go?

Pulsenomics’ Home Price Expectation study – a study of over one hundred economists, real estate specialists, investment and market strategists – is one reputable source of that information.

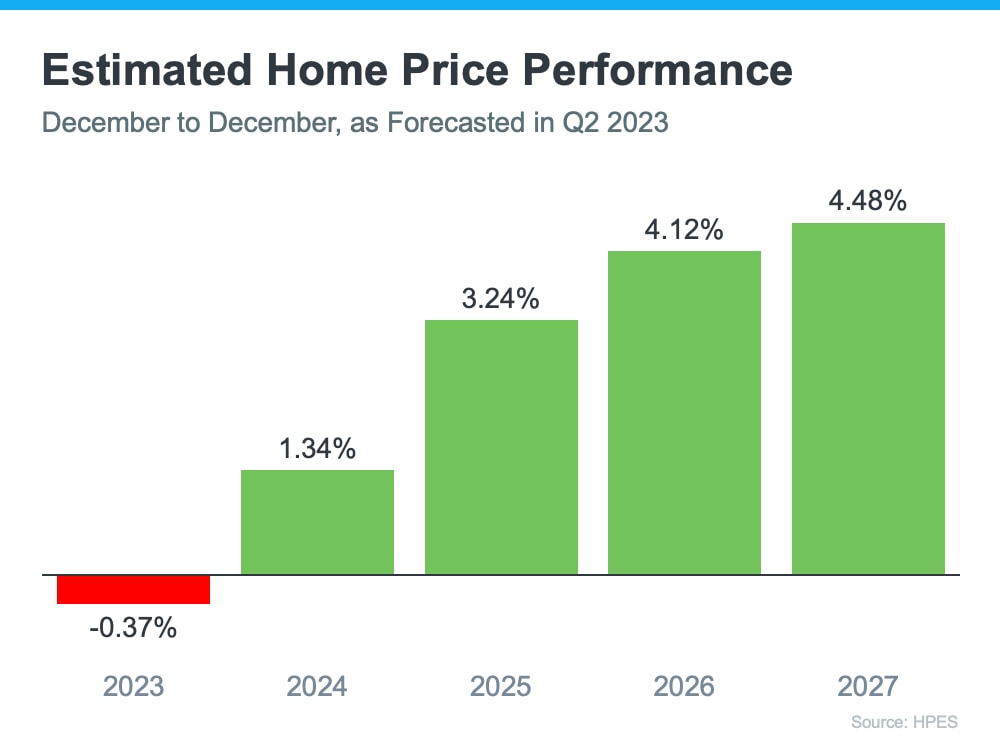

According to the most recent release, the experts polled predict a small depreciation this year (see red in the graph below). But here’s the most important context. The worst of the home price drops are now behind us, and prices are beginning to rise again in many cities. Not to mention, the 0.37% depreciation shown by HPES for 2023 is far from the crash that some predicted would occur.

Let’s turn our attention to the future. The green in the graph below indicates that prices have turned a corner and will rise in 2024 and beyond. The HPES predicts that after this year, home price appreciation will return to more average levels for the next several years.

So, why is this important to you? It means that your home’s worth will likely rise and you will build equity in the years ahead, but only if you buy now. Based on these projections, waiting will only cost you more money in the long run.

Where Do I Think Mortgage Rates Will Go?

Mortgage rates have risen in response to economic uncertainty, inflation, and other factors over the last year. According to the most recent reports, inflation, while still high, has slowed since its peak. This is a positive indicator for the market and mortgage rates. This is why.

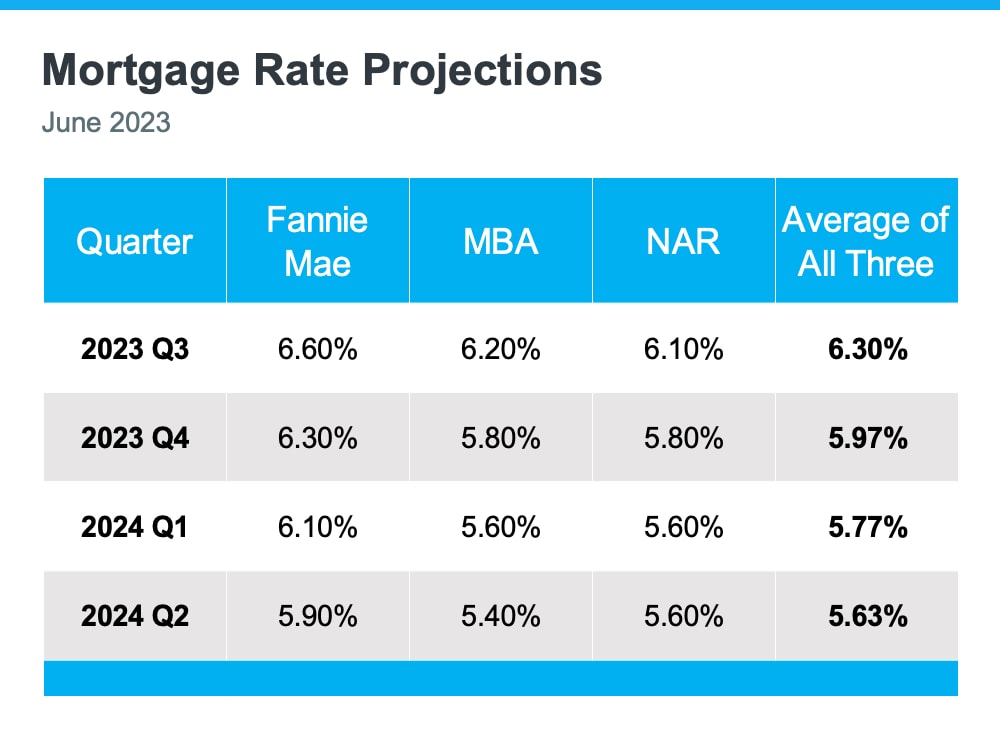

When inflation falls, mortgage rates tend to reduce as well. This could be why some analysts predict that mortgage rates will fall slightly over the following few quarters, settling somewhere between 5.5 and 6% on average, but that remains to be seen with rates now staying above 7% and may very well go to 8% or higher!

But no one, not even the experts, can predict where mortgage rates will be next year or even next month. This is because there are so many variables that might influence what happens. So, to give you a glimpse of the potential outcomes, consider the following:

If you buy now and mortgage rates do not change: You made a solid decision because home prices are expected to rise over time, so you beat rising prices.

If you buy now and mortgage rates fall (as predicted): you will have made a good decision because you bought before home prices increased. You can always refinance your house later IF interest rates fall.

If you buy now and mortgage rates rise: If this occurs, you made an excellent decision because you purchased before both the price of the home and the mortgage rate rose.

Summing It Up

If you’re considering buying a house, you should be aware of the current state of housing prices and mortgage rates. While no one can predict where they will go, real estate professionals can provide you with useful information to keep you informed. If you’re considering buying a home in Cobb County or the Metro Atlanta area and have questions just get in touch – (404) 410-6465 or visit Complete Realty Team to contact us by email.

According to Bankrate and Freddie Mac, the current average interest rate for a 30-year-fixed mortgage is 7.58%, which is the highest it has been in over 20 years. Experts are now predicting that this could go up to 8%, if the economy continues to show signs of strength and the Federal Reserve raises interest rates again. If this happens, the housing market could go back into a deep freeze.

Lenders have guidelines regarding max DTI to approve a loan.

Many lendaers allow for DTI ratios up to 50%.

Still, loans with higher DTI ratios typically have worse terms.

Higher DTI may require a higher down payment to meet loan approval criteria.

U.S. mortgage rates are inching closer to 8%, a two-decade high, making homeownership increasingly out of reach for many Americans. The Federal Reserve's aggressive tightening campaign against inflation is causing upward pressure on market rates, making existing home sales slump further and potential first-time borrowers hesitant. Lawrence Yun, chief economist at the National Association of Realtors, believes mortgage rates could go higher than 8%, but also that the current high may be the peak before it retreats. In contrast, mortgage rates averaged 16.63% in the past. Perry Johnson, a Republican presidential candidate, filed a complaint with the

According to Bankrate and Freddie Mac, the current average interest rate for a 30-year-fixed mortgage is 7.58%, which is the highest it has been in over 20 years. Experts are now predicting that this could go up to 8%, if the economy continues to show signs of strength and the Federal Reserve raises interest rates again. If this happens, the housing market could go back into a deep freeze.

Check out our latest video – What’s Going To Happen With Mortgage Rates:

So you’ve undoubtedly seen some news concerning inflation and mortgage rates, as well as something about a Federal Reserve (the Fed) decision. You may be wondering what it all means for you, especially if you’re considering purchasing a home. Allow me to break it down for you.

The Housing Market and Inflation

The Fed is working really hard to reduce inflation. Even if the most recent figures show modest improvement, the inflation rate remains above the 2% target. One of the reasons the Fed chose to raise the Federal Rate again was because of this. According to Bankrate, the Fed has hiked interest rates for the tenth time in ten meetings to combat inflation and cool the economy, which has been growing since rebounding from the 2020 coronavirus recession.

The Fed’s activities do not directly affect mortgage rates, but they do have an impact. Their actions last year contributed to a purposeful downturn in the residential real estate market.

What Impact Does Rates And Inflation Have on You?

Everyday expenses, such as gas and groceries, are becoming more expensive as a result of high inflation. You’ve probably already observed this, especially at the Grocery store!! The Fed is attempting to reduce inflation by hiking the Federal Funds Rate. If they are successful, it may result in lower mortgage rates, making house ownership more accessible for you. This is because when inflation is high, so are mortgage rates. Experts predict that if inflation slows, mortgage rates will follow suit.

The problem is that Biden’s Administration has gone after America’s fossil fuel production. Here at Complete Realty Team we are all for having a cleaner planet, but it will take time to do so. We can’t stop our dependence on fossil fuels overnight. It takes energy to produce everything from the clothes on your back to the food on your table!

What Do Experts Expect to Happen Next?

Inflation and mortgage rates will continue to have an impact on the housing market in the future. According to Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), mortgage rates will likely fall later this year as consumer price inflation moderates. Mortgage Bankers Association (MBA) Chief Economist Mike Fratantoni concurs, predicting that mortgage rates will fall this year as the economy slows.

Nobody knows what will happen to mortgage rates, but analysts believe they will fall this year if inflation falls as well. Connect with a reputable real estate advisor if you want to stay informed. They are aware of what is going on and can assist you in understanding what the experts are predicting and how it may affect your plans to purchase a home.

Summing It Up

Don’t be perplexed by the recent Federal Reserve decision. What happens to mortgage rates is determined by the rate of inflation. Mortgage rates will fall if inflation cools off, but will go up if inflation continues.

Our take – rates are probably going to go up with the Fed already hinting at raising rates at least one more time this year. The last stat we saw is that inflation was at 3.2% with their target being 2%.

If you have questions, want to know your home’s value or to buy or sell a house, just visit Complete Realty Team or give us a call at (404) 410-6465. You can also go here to get more real estate news VIDEOS.

Plan your finances and consult an advisor before house hunting to set a budget within 30-35% of your income.

Define must-have features based on lifestyle and plans to streamline the home-searching process after budgeting.Mortgage pre-approval helps serious buyers determine affordability, compare lenders, and gain a competitive edge.

Mortgage rates have been steadily increasing for the past six weeks, causing a slight dip in home purchases and an increase in the available inventory of homes for sale. The economy is strong and the Federal Reserve is expected to keep rates high for longer, further increasing monthly payments and making home buying less affordable. Inventory is expected to peak at the end of August, with 20% fewer homes on the market than in 2022.

This article discusses the financial obligations of both homeowners and renters, and how to determine if you can afford to buy a house. Homeowners have to pay more than just their monthly mortgage payments, such as taxes, insurance, and repairs. On the other hand, renters usually only need to pay their monthly rent and a deposit when they move in, along with optional pet or cleaning deposits. It is important to consider all of the costs before deciding to become a homeowner.

Avg home price/sq-ft in Middle Georgia increased to $123 from $118, reflecting recent growth.

A 2,058 sq-ft home on Ashford Chase Court sold for $255K, indicating market activity.

Figures based on sales from July provide current trend insight.

Recent data suggests ongoing price fluctuations in Middle Georgia's housing market.

Homeowners pay $14,144 yearly, or $1,180 MoM, for bills, taxes, insurance, and maintenance on top of their mortgage.

Nationally, property taxes, homeowners insurance, and utility payments avg $7,742.

Georgia's buyers can save $30K by building instead of buying a home.

The estimated cost to build a home in Georgia is $365K.

The median home price in Georgia is $395K.

Despite earning a salary of $100,000, which is higher than the national median household income, 49% of people still find it difficult to buy a home. The 28/36 rule suggests spending no more than 28% of your income on housing expenses and no more than 36% on total debt payments. This means that on a salary of $100,000, the mortgage payment should be no more than $2,333 and other debts should be no more than $667 per month. Other variables such as savings, homeowners insurance and property taxes also need to be taken into account. A 20% down payment on a $400

Today's market is tough for many prospective homebuyers, with mortgage rates on average around 6-7%, and a shortage of homes for sale pushing up prices. However, for some buyers, now can still be a great time to buy. Plus, you can start building equity in your home and plan to refinance in the future.