Halloween falls on October 31 because the ancient Gaelic festival of Samhain, considered the earliest known root of Halloween, occurred on this day.

In the eighth century, Pope Gregory III designated November 1 as a time to praise all saints.

Soon, All Saints' Day incorporated some traditions of Samhain and the evening before was known as All Hallows Eve, and later Halloween.

Over time, Halloween evolved into a day of activities like trick-or-treating, carving jack-o-lanterns, festive gatherings, donning costumes and eating treats.

Today’s the day to eat candies and sweets to your heart’s content! Happy Halloween!

The Georgia Department of Community Affairs is opening applications for the Housing Choice Voucher Program.

This program, funded by HUD, aims to assist low-income families and individuals in obtaining safe and sanitary housing.

Eligibility for the program is based on factors such as total annual gross income, family size, and immigration status.

The Housing Choice Voucher Program in Georgia will open its applications for the waitlist for three days in October, allowing families who need assistance covering their rent to apply. A lottery system will be used to select who will be added to the waitlist and those selected will be randomly placed on the list to get a housing voucher. The Department of Community Affairs is also looking for renters to join the program which can be done online.

With mortgage rates at 7.67%, buying a home may not be the most financially viable option. The Mortgage Bankers Association reports that while the average 30-year fixed rate mortgage is at a high, the rate on the average 5-year adjustable-rate mortgage (ARM) actually went down to 6.33%. This has caused a surge in ARM applications, and is the highest since November 2022. Real estate experts explain the current housing shortage in part by pointing to baby boomers who are staying in their homes longer and a decrease in homebuilding activity. For those looking to buy now, the ARM may be the best option,

The housing market in September showed a decrease in actively listed homes, newly listed homes, and total unsold homes compared to last year. However, the median price of homes for sale increased slightly, and the inventory of homes for sale increased from August. Despite this, total listings were still 12.2% lower than the same time last year, leaving buyers to contend with higher listing prices, mortgage rates, and lower inventory.

Ken Mandich from Complete Realty Team has published a new blog post and YouTube video discussing the recent rise of adjustable-rate mortgages (ARMs) and whether they can be a good choice for some homeowners.

Adjustable-rate mortgages were extremely popular at the beginning of the 21st century. Notably, many experts believe that their popularity was in part responsible for the 2008 housing market crisis. However, today, after many years of inactivity, homebuyers are being presented with the option of going for adjustable-rate mortgages again for their home purchases.

Ken describes the benefits of ARMs by saying, “With an adjustable-rate mortgage, homeowners make lower monthly payments at the beginning and the rate goes up several years into the duration of the mortgage. This helps homebuyers to get started with their dream of homeownership with favorable rates with an expectation that their income will keep up with the increased rates in the future.”

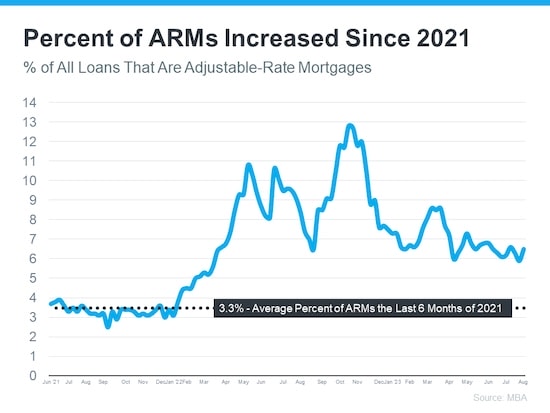

According to statistics from the Mortgage Bankers Association (MBA), in the last 6 months of 2021, around 3.3% of all mortgages issued in the United States were adjustable-rate mortgages. There was a spike in the number of ARMs approved in 2022 with the number finally settling to around 6.5% in the first half of 2023.

Ken talks about the reasons why ARMs have a slight uptick by saying, “It’s simple. Mortgage rates have increased considerably in the last year. With rising rates, several homeowners chose ARMs since standard prices were high and they provided them with a lower rate.”

Despite ARMs being very popular for many homeowners, this resurgence may have also evoked flashbacks to the 2008 crisis. However, the banks and mortgage providers have learned their lessons and are being more selective of who qualifies for ARMs. In the early 2000s, banks and mortgage providers were playing fast and loose with the rules. On the other hand, today, they are seeking verification of employment, assets, incomes, and so forth to make their decisions.

“I realize that ARMs get a bad rap as they conjure up images of the 2008 subprime mortgage crisis that destroyed millions of lives across the nation,” says Ken Mandich. “This time, things are different. Back then, mortgage providers were callous in their conduct and offered mortgages to pretty much anyone who applied. Today, they are doing their due diligence and asking for the right documentation as proof to ensure their customers have the ability to pay off their mortgages in the future. So, there is no fear of ARMs causing another housing crash.”

Ken Mandich, who has called the North Metro area home for over 30 years now, has over a decade of experience being a real estate investor and house flipper. As a REALTOR® and part of the ERA Sunrise team, Ken Mandich helps his clients get straight answers to their questions and delivers proven results. He is intimately familiar with the real estate market in Cobb County and the metro Atlanta area and can help his clients with everything from downsizing, relocating, selling, buying, investing, or even buying their first home in Georgia.

Ken and Complete Realty Team help clients with every step of the real estate transaction process including comparable home price analysis, open houses, property surveys, HOA agreements, credit reports, title companies, lenders, homeowners’ insurance, walk-throughs, terms of sale or purchase, concessions, repairs, and closing documents.

“Our ERA team’s innovative marketing strategies, negotiation skills, and local market knowledge have allowed us to consistently help our clients sell their property for top market value as quickly as possible, as well as help buyers find their perfect dream home or investment property. So, if you are ready to buy a home in Cobb County, give me and my team a call today,” says Ken Mandich.

https://www.youtube.com/watch?v=P_MFXXdhBpA

Readers can contact Ken Mandich at (404) 410-6465 or admin@completerealtyteam.com to get started with finding and moving into their dream property in Cobb County and the Metro Atlanta area. For more real estate news, homebuyers and homeowners are urged to follow his YouTube channel.

Mid-Q3 saw a slowdown in Real Estate activity, while the housing market experienced rising prices and decreasing inventorySales and Inventory:

New Listings: ↓7% to 16,054

Pending Sales: ↓15% to 10,640

Closed Sales: ↓12% to 11,468

Inventoary: ↓4% to 27,387

Prices and Days on Market:

Median Sales Price: ↑3% to $356,688

Average Sales Price: ↑6% to $427,639

Days on Market: 35

Last week, US mortgage rates topped 7.5%, the most since mid-August, and applications for home purchases tumbled to a multi-decade low. This illustrates the battered housing market, caused by aggressive interest-rate hikes by the Federal Reserve, soaring bond yields, and rising mortgage rates and home prices. This has created one of the most unaffordable housing markets on record. The Federal Reserve is likely to keep interest rates elevated for the foreseeable future to tame inflation.

Mortgage rates have recently hit a two-decade high, with the 30-year fixed-rate average at 7.87%, the 15-year rate average at 7.18%, and the jumbo 30-year rate at 7.15%. It is important to shop around for the best mortgage option and compare rates regularly, as refinancing rates have moved differently from new purchase rates.

Home inspections are crucial in Georgia to assess a property's condition, uncover potential issues, and negotiate repairs or credits.Specialized inspections like radon testing and sewer scopes are recommended, especially in areas with elevated radon levels.

Home inspections are not required in Georgia but are highly recommended, and it's wise to hire licensed and certified inspectors.a

Experts generally rule out a housing market crash in Georgia.

Fewer new listings and closed sales indicate a cooling market.

High demand continues to push prices upward.

Should You Be Concerned About the Reintroduction of Adjustable-Rate Mortgages?

If you recall the 2008 housing meltdown, you may recall how popular adjustable-rate mortgages, (also known as an ARM). And, after years of being nearly nonexistent, ARMs are becoming increasingly popular when buying a home. Let’s look at why this is happening and why it’s not a cause for alarm.

Why Have ARMs Become More Popular Recently?

This graph uses Mortgage Bankers Association (MBA) data to demonstrate how the share of adjustable-rate mortgages has increased in recent years:

As shown in the data, after hovering around 3% of all mortgages in 2021, many more homeowners switched back to adjustable-rate mortgages last year. That growth has a straightforward reason. Mortgage rates increased considerably last year. With rising borrowing rates, several homeowners chose this sort of loan since standard borrowing prices were high, and an ARM provided them with a lower rate.

Why Are Today’s ARMs Not The Same As Those In ’08?

To put things into perspective, keep in mind that these aren’t the ARMs that were popular in the run-up to 2008. Loose lending rules contributed to the housing meltdown. When a buyer obtained an ARM, banks and lenders did not check verification of employment, assets, income, and so forth, people could get a loan without having to prove anything! Essentially, people were receiving loans that they should not have received. Many homeowners were put in jeopardy as a result of their inability to repay loans for which they were never required to qualify in the first place.

Lending requirements are different this time. Banks and lenders learned from the crash, and they now verify income, assets, employment, and other information. This implies that today’s buyers must qualify for their loans and demonstrate their ability to repay them.

CoreLogic Economist Archana Pradhan outlines the difference between then and now:

“Around 60% of Adjustable-Rate Mortgages (ARM) that were originated in 2007 were low- or no-documentation loans . . . Similarly, in 2005, 29% of ARM borrowers had credit scores below 640 . . . Currently, almost all conventional loans, including both ARMs and Fixed-Rate Mortgages, require full documentation, are amortized, and are made to borrowers with credit scores above 640.”

In plain terms, Laurie Goodman of the Urban Institute emphasizes this idea by saying:

“Today’s Adjustable-Rate Mortgages are no riskier than other mortgage products and their lower monthly payments could increase access to homeownership for more potential buyers.”

Summing It Up

If you’re concerned that today’s adjustable-rate mortgages will be similar to those used during the housing meltdown, rest assured that things are different this time. If you have questions about buying or selling a home in the Metro Atlanta area, we’d be more than happy to help! Just reach out to us at (404) 410-6465 or visit Complete Realty Team. We look forward to speaking with you!

The housing market in October is not looking any different from the current market, with mortgage rates remaining high and limited inventory. Home prices are also expected to continue to rise, making it even more difficult for buyers to afford. However, despite the challenge, it is still possible to buy a home in October.

FSBO involves a series of steps that homeowners need to undertake independently.

FSBO is time-consuming, involving market analysis, home staging, marketing, negotiation, and legal tasks.Lack of Real Estate knowledge can lead to costly errors in understanding market trends, laws, and negotiation tactics.

Even if the housing market has calmed from the frenzy of the ‘unicorn’ years, it remains a seller’s market due to the scarcity of available properties. But what does this mean for you? And why are conditions so favorable today if you want to sell your home?

According to the National Association of Realtors’ (NAR) most recent Existing Home Sales Report, housing supply remains astoundingly low. The quantity of available properties on the market is used to calculate housing inventory. It is also quantified in months’ supply, which is the number of months required to sell all available properties based on current demand. A six-month supply is typical in a balanced market. At the present sales rate, we only have roughly 3 months’ supply of homes or less in some areas (see graph below):

Given the existing availability of properties, it’s still a seller’s market, as the graph illustrates.

We’re still a long way from having a balanced market. In reality, the current months’ supply is half of what a normal market would have. Based on current buyer demand, this indicates there simply aren’t enough properties to go around.

“There are simply not enough homes for sale. The market can easily absorb a doubling of inventory.”

What Are the Advantages of Being in a Seller’s Market?

Sellers, these conditions provide you a significant advantage. There are home buyers chomping at the bit that are ready, willing, and able to buy a home right now. And, because there are fewer homes for sale, those that do come on the market act as magnets for those buyers.

If you enlist the help of a local real estate agent to market your house, that’s in good condition, and priced correctly, it could attract a lot of interest. You may even receive many offers!

But hold on! Are there more houses on the market?

If you’re debating whether or not you should sell your home, well, you may not have another great opportunity as this for quite some time, it’s one of the most significant advantages you have right now. When housing availability is this limited, your home will stand out, particularly if it is reasonably priced. We can’t overstress that enough. With interest rates being so high buyers are NOT willing to overpay for a home.

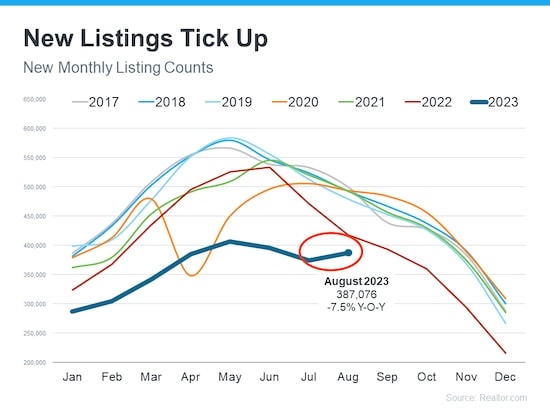

However, there are some early indications that additional listings are on the way. According to the most recent data, new listings (homeowners who have recently listed their home for sale) are on the rise. Here’s why this is significant and what it might mean for you.

There Are More Homes Being Listed For This Time Of Year

The spring buying season is well recognized to be the busiest time of year in the housing market. As a result, the number of newly listed residences increases predictably throughout the first half of the year. Sellers are bracing for this and preparing for the months when buyers are most active. However, when the school year begins and the holidays approach, the market cools. It’s to be anticipated.

But here’s the surprising part. According to the most recent Realtor.com data, there is an uptick in the amount of sellers advertising their homes later this year than typical. A high this late in the season is unusual. In the graph below, you can observe both the normal seasonal tendency and the extraordinary August:

“While inventory continues to be in short supply, August witnessed an unusual uptick in newly listed homes compared to July, hopefully signaling a return in seller activity heading toward the fall season . . .”

While this is only one month of data, it is noteworthy. It’s still too early to tell if this trend will continue, but if it does, you’ll want to be prepared.

What Does This Mean for Home Sellers?

If you’ve been putting off selling your home, this could be the perfect time. That’s because, if this tendency continues, the longer you wait, the more competition you’ll face. If your neighbor also lists their property for sale, you may have to compete for the attention of buyers with that other homeowner. If you sell today, you will be able to outbid your neighbors.

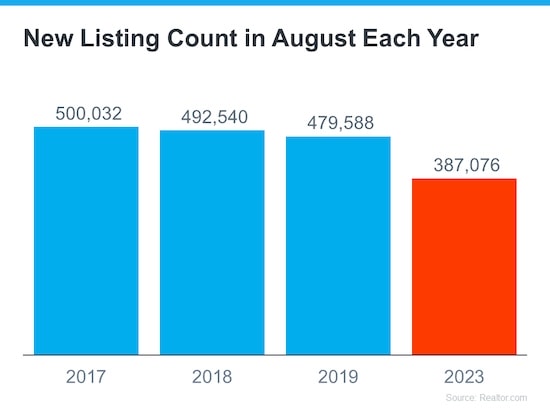

Even with more properties on the market, the market remains far below normal supply levels. And the inventory shortfall won’t fix itself overnight. The graph below helps put this into context, allowing you to realize the opportunities you still have right now:

Summing It Up

You don’t want to wait for more competition to appear in your community, even if inventory is currently low. If you sell your house now, you will still have a fantastic chance. Let’s talk about the advantages of selling now, before more houses hit the market. If you’re ready to sell your house, have questions about what it’s worth or any other questions, just give us a call. You can reach us at (404) 410-6465 or visit Complete Realty Team. We look forward to hearing from you!

As of mid-2023, the predicted recession has not materialized, and the economy is in a state of flux.

While there are signs of a slowdown, the forecast for a recession has been pushed further out.

Indigenous Peoples’ Day celebrates, recognizes, and honors the beautiful traditions and cultures of the Indigenous People

We take a stand for and support the indigenous people on this day.

We should also offer our support to those who invest and uplift the indigenous communities.

Mortgage interest rates [↑](color-green) 2X since 2021, now averaging 6.78% for a 30-yr fixed-rate loan.

Choosing the right mortgage lender is challenging due to numerous options and mortgage types.